Get the edge over other buyers, and a $10,000 seller guarantee

I Want the Edge!

The first thing you should do is find out how much house you can afford. Once you know your estimated home affordability, you can start building your personalized home buying team.

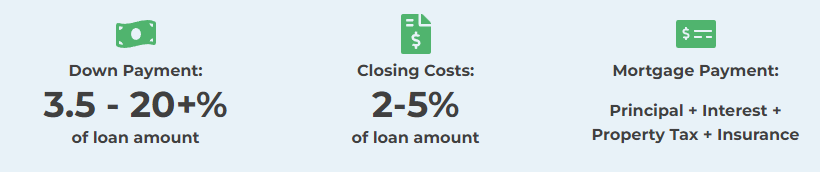

The true cost of a mortgage is just not your monthly mortgage payment. Here are the most common fees that go into your mortgage so you’ll know what to expect.

Down Payment: Cash that you will pay up front on the final price of your home before the mortgage starts.

Principal: The amount you of money you borrow when you get your home loan. To calculate your principal, subtract your down payment amount from the home's purchase price.

Interest: The amount you are being charged in order to borrow money from a lender. Interest is based on your principal amount. So, if you pay $350,000 in principal with a 7% interest rate, you'll pay about $24,000 each year until your loan is paid off.

Insurance: Homeowner’s insurance is required. Private Mortgage Insurance (PMI) is for conventional home loans when you pay less than 20% toward your down payment. You will pay Mortgage Insurance Premiums (MIP) if you have an FHA loan.

Closing Costs: These costs are part of your final contract. Most home buyers pay 2-5% of the loan amount in closing fees which usually include: application fee, processing and insurance fees, property taxes, and title company expenses.

The most important part of understanding the mortgage process is finding a lender who understands you and your home loan goals (like saving time and money). Some parts of the process can be taken care of now while other parts will occur after you’ve picked out your home.

Here’s a quick and easy view of the home loan process: