Download our go-to resource for a mortgage that won't bust your budget!

As a Dave Ramsey fan, you understand the importance of financial stability and staying out of debt. At Churchill Mortgage, we’re here to help guide you toward the real American Dream, debt-free homeownership, so you can own your home free and clear!

Refinancing your home has never been easier (or faster)! And now may be the perfect time to save money. We can help you avoid common refinancing pitfalls that many homeowners experience.

What Does it Mean to Refinance a Mortgage?

Refinancing is the process of getting a new mortgage so you can lower your interest rate, reduce monthly payments, remove mortgage insurance, or change your loan term or loan type.

Why Should I Refinance?

The number one reason people refinance is to lock in a lower interest rate. Why? This can potentially save you hundreds to thousands off your total mortgage payment.

You may not realize there are other great reasons to refinance:

Remove PMI

If your original down payment was less than 20%, you are probably paying Private Mortgage Insurance. Your home could now have enough equity to refinance and remove it.

Change Your Loan Term

You may want to adjust your term (i.e. 30-year to a 15-year loan) to save money on interest and build wealth. This is a great option if you want to own your home free and clear.

Switch Your Loan Type

If you currently have an FHA loan or an Adjustable Rate Mortgage, it may be worth looking at conventional, fixed-rate mortgage options to help you save money long-term.

Lower Your Monthly Payment

A lower monthly payment is typically achieved by refinancing into a lower interest rate or a longer loan term. This can affect the amount of interest you pay, so it’s important to know the total cost of your mortgage when refinancing.

By shortening the term of your loan (and making fewer total payments), you can reduce the overall amount of interest you'll pay over the life of the loan. A lower interest rate can also help lower the amount of total interest paid when refinancing.

It is important to see if you can benefit from any of these refinancing reasons so you can align your mortgage with your financial goals. Contact us if you need help with the next step!

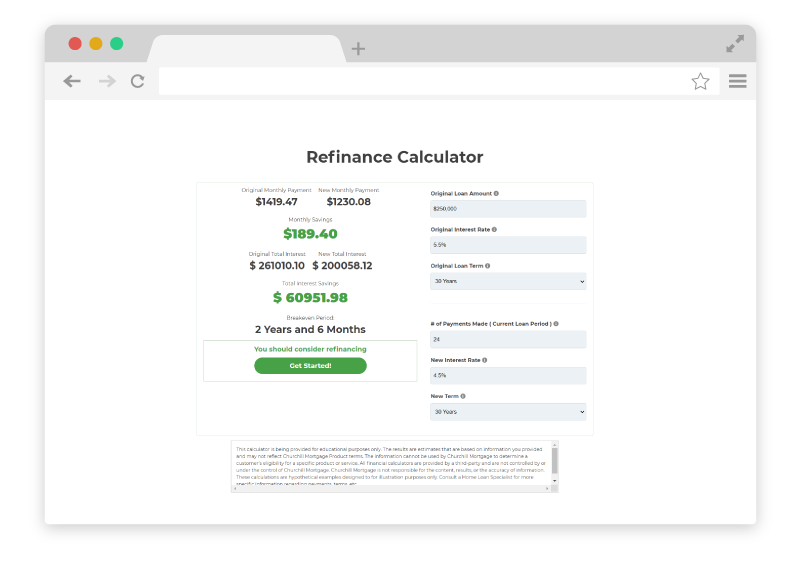

Refinance Calculator

This calculator is being provided for educational purposes only. The provided values for interest rates are examples only and do not reflect Churchill Mortgage Product terms & offers. The results are estimates that are based on information you provided and may not reflect Churchill Mortgage Product terms. The information cannot be used by Churchill Mortgage to determine a customer's eligibility for a specific product or service. All financial calculators are provided by a third-party and are not controlled by or under the control of Churchill Mortgage. Churchill Mortgage is not responsible for the content, results, or the accuracy of information.These calculations are hypothetical examples designed to for illustration purposes only. Consult a Home Loan Specialist for more specific information regarding payments, terms, etc.

When buying a home, you’ll probably have a lot of questions. The first thing you should do is find out how much house you can afford. We provide an easy-to-use calculator utilizing your monthly income with your projected loan term.

Dave recommends:

Have a down payment of at least 10%

Spend 25% or less of your monthly net pay

Get a 15-year fixed-rate mortgage

Once you know your estimated home affordability, you can start building your personalized home buying team.

Lowering Your Rate Could Save You Thousands

Because the interest rate on your home loan is directly tied to how much you pay on your overall mortgage, lower rates usually mean lower monthly payments.

Check out this example of monthly payments (principal and interest) on a 15-year fixed-rate loan of $250,000 at 5.5% and 4.0%.

Total Interest at 5.5% = $117,687

Total Interest at 4% = $82,860

With a 1.5% difference in interest rate, there is a $34,827 difference in interest paid! Imagine what you could do with that in your pocket!

* The scenarios listed above have an APR of 5.5% and 4% respectivly. Additional fees are not included in the examples above.

With so much of your hard-earned money on the line, it’s best to seek advice from a trusted home loan expert and have the confidence that you are in qualified hands.

Refinance to a Smarter Mortgage

Paying off your current mortgage is one of the data points of an everyday millionaire. Get more power, clarity, and peace throughout the entire refinancing process to help you get back to a debt-free lifestyle as soon as possible.

The right time to refinance looks different for everyone. So, take time to run the numbers with a Dave Ramsey Mortgage Expert and get your break-even analysis. You want to make sure it makes sense for you and your unique situation to refinance now.

The Churchill Mortgage app is easy to navigate and keeps you up-to-date as key refinancing milestones are checked off.

It’s easy to engage with a Dave Ramsey Mortgage Expert when you want, how you want, and from where you want!

Upload key documents securely anytime, anywhere

Stay connected to your home loan team

Monitor your progress, every step of the way

FAQs

Have a Refinancing Question?

Looking for answers to your questions about refinancing? We have you covered. Learn more about loan terms, loan applications, documentation needed, no score loans, and much more.

A:

Refinancing is when you pay off an existing home loan and replace it with a new one.

A:

Most people refinance their mortgage to save money. That may look different depending on your situation, but most people want to remove Private Mortgage Insurance (PMI), reduce their loan term, or switch their loan type.

A:

Yes, you can! This is part of our Churchill Checkup. Visit the page for more information on how to get your free report and schedule a quick call with one of our expert Home Loan Specialists to discuss your refinancing goals.

A:

You can download our free Refinancing Starter Kit here. This guide will give you 5 simple steps to refinance your home and paying off your home loan.

A:

A lot of weight is put on a FICO® Score because it’s an easy way to do a quick risk assessment. If you don’t have a FICO® Score it can make qualifying for a mortgage a little more difficult, but not impossible. Many lenders do not offer no credit score loans.

A:

Yes, Churchill Mortgage accommodates this type of loan on a regular basis with expertise. We work hard to make sure you are not penalized for non-traditional credit. Our Home Loan Specialists are professionally trained to help you get a smarter mortgage that can be paid-off quickly, so you can return to a debt-free lifestyle as soon as possible.

A:

Typically, you must have four alternative credit tradelines with the most recent consecutive 12-month payment history from the creditor stating each were paid on time. Examples of alternative credit can be: cell phone bills, utility bills, insurance that’s paid monthly or quarterly (but not payroll deducted), school tuition, child care, or rent payments. If you are living rent free, a conventional loan without a 12-month rental payment history will require 12 months of assets to cover your principal and interest (P&I), taxes, property, flood, and mortgage insurance premiums. Click here to download our How to Buy a Home with Zero

A:

We’ve found that a 15-year fixed rate loan with a 20 percent down payment gives you the best chance for approval. This type of loan eliminates the need for private mortgage insurance (PMI) and presents a lower risk to the loan servicer.

A:

With no credit score available, an underwriter will go through your documentation to establish a history of payments for alternative credit. Don’t look for quick answers during this process. It can take about three times longer than a normal borrower file and sometimes additional documentation will be requested. Give your underwriter at least 60 days to look into the loan risks before issuing approval. Your Home Loan Specialist is always available to give a more detailed timeline for the underwriting process and to assist writing a contract closing date.

A:

Don’t sign any sales contracts for a home purchase without protective contingencies to cover you in the contract. You’ll also want to make the sale contingent upon being fully approved, otherwise all earnest money can be returned to the buyer. Stay away from any 100 percent commitments until you know your loan has been “cleared to close” and there aren’t any other conditions needed.

A:

Dave Ramsey recommends a 15-year, fixed-rate conventional loan. A conventional loan is not secured by a government agency, making it a little trickier to qualify if you don’t have a credit score. Requirements for a conventional loan with no credit score means you need at least 12 months of flawless payment history on eligible monthly bills, and you may also need to take a homeownership education class. If you do qualify for a conventional loan the benefits far outweigh the effort needed to qualify! We do have other no score loan options ranging including but not limited to FHA and VA.

A:

Churchill Mortgage and Dave Ramsey are closely aligned through shared principles and core values. The two teams work together to help Americans buy homes the smart way and ultimately become debt-free. This is what we call the real American Dream. Churchill is the only lender that does that, and therefore, the only lender the Dave Ramsey talks about on his show.